BY James Williams

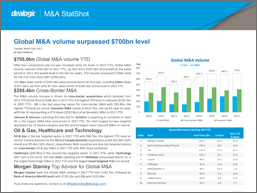

Global dealmaking remains “resilient” in the face of an uncertain year, according to Mergermarket’s new ‘Global and regional M&A: Q1 2017’ report, which reveals a year-on-year increase in deal value of 8.9 percent.

The report, which confirms that global business making remains buoyant despite the prospect of an uncertain 12 months, shows that consumer mega-deals reached a record value during Q1, with 395 deals worth $136.1bn agreed.

“The consumer sector stole the limelight in Q1, with a record three deals over $10bn,” said Katharine Dennys, research editor at Mergermarket. “Deals such as BAT/Reynolds, Luxottica Group/Essilor International and Mead Johnson/Reckitt Benckinser caused Q1 value to account for almost two-thirds of total 2016 consumer activity.”

The report also states that, due to stricter regulations being imposed on transactions, Chinese dealmakers had a ‘reversal of fortunes’ in terms of their outbound investment, with the 96 deals worth $82bn in Q1 2016 reduced to 75 deals worth $11.8bn, an 85.6 percent drop in value. “Coupled with increased protectionism from the US and UK, this may signal the end of China’s outbound acquisition spree, at least in the short-term”, suggests Ms Dennys.

Due to the UK’s exit from the European Union, political uncertainty appears to have discouraged international dealmakers from pursuing transactions in the region. Despite this, US dealmakers had a strong quarter investing in the continent, with 150 deals worth $55.7bn – a 16 percent uptick in value compared to Q1 2016 (176 deals worth $48bn) and the strongest Q1 deal value posting since 2008 (138 deals worth $112.6bn).

Uncertainty throughout Europe has also seen inbound investments take a hit, with the report noting that value was reduced to 55.7 percent in comparison to Q4 2016. Furthermore, against a backdrop of Brexit negotiations and upcoming elections in France and Germany, Q1 saw 262 deals worth $71.7bn – the slowest by value since 2014 (291 deals worth $55.8bn).

Ms Dennys concluded: “There is evidence to suggest that dealmakers are seeing deals as more precious, with larger sums being invested in fewer deals. This is reflected in the average size of disclosed value deals reaching its highest Q1 level on Mergermarket record.”

Report: Global and regional M&A: Q1 2017